The Real Estate Transaction Tax has directly reshaped how property is priced, documented, and transferred in Saudi Arabia. Since it was introduced as a replacement for VAT on real estate disposals, it has moved from specialist legal terminology to a routine step that anyone buying or selling property must navigate. Ignorance of its provisions does not create an exemption from them; understanding this tax is a non-negotiable part of any real estate transaction.

Ayqan Law Firm provides specialist legal advice on real estate transaction tax, including eligibility for available exemptions across different types of property disposals.

What Is the Real Estate Transaction Tax in Saudi Arabia?

Definition, Legal Basis, and Royal Order No. A/84

The Real Estate Transaction Tax is a levy imposed on transactions that transfer ownership of real property or rights of usufruct. It was enacted under Royal Order No. A/84 and applies broadly to sales, gifts, exchanges, and other disposals. It is administered by the Zakat, Tax and Customs Authority (ZATCA) and is collected at the point of electronic registration of the transaction. Our tax practice works alongside our real estate team to align each transaction with these requirements from day one.

Why It Was Introduced Instead of VAT on Real Estate

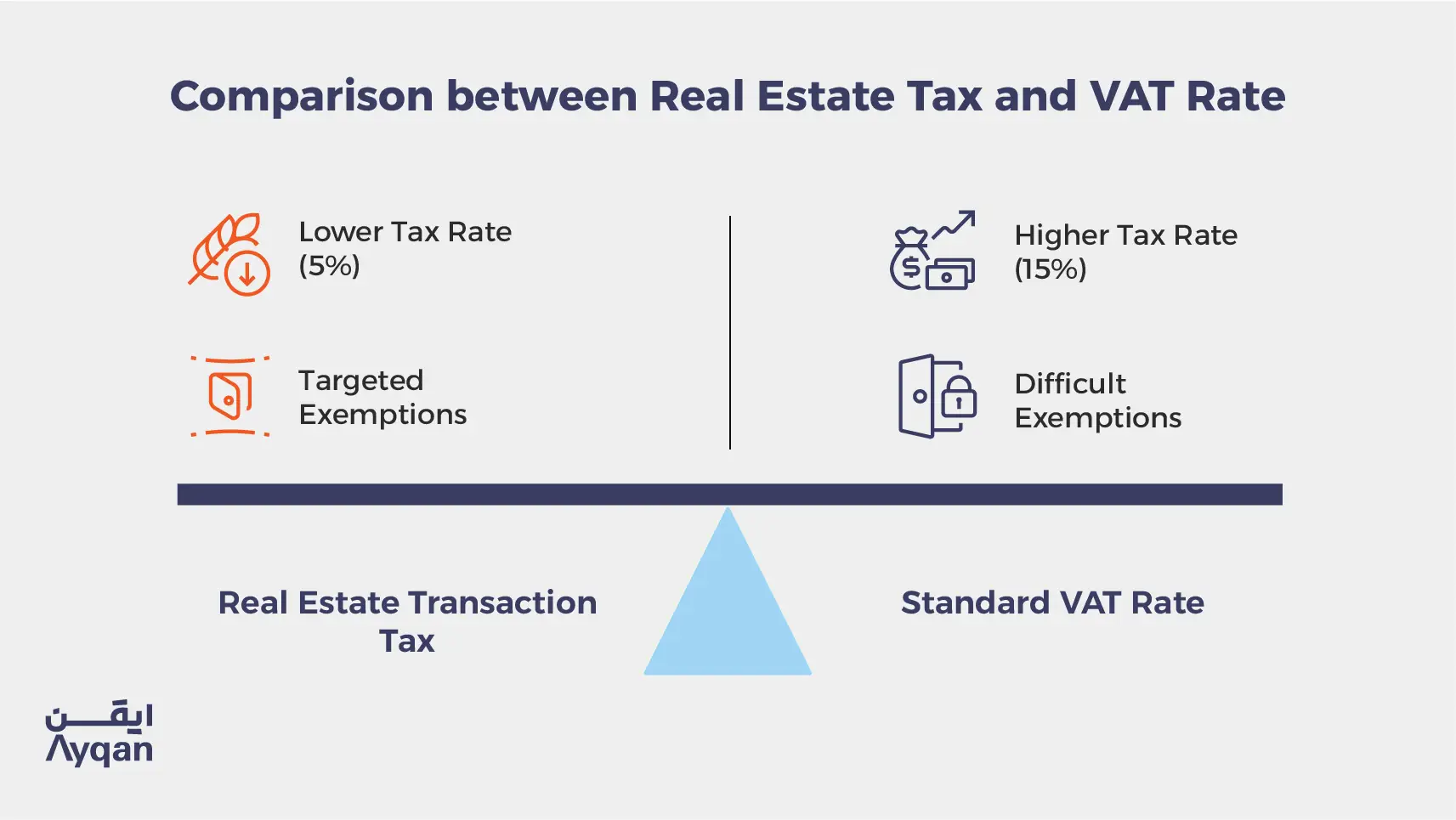

Rather than subjecting real estate transactions to the standard 15% VAT rate, Saudi Arabia chose to apply a dedicated Real Estate Transaction Tax at a rate of 5% of the transaction value. This policy choice reduces the tax burden compared to the alternative and, crucially, makes it possible to apply targeted exemptions, such as the first-home exemption for Saudi citizens, that would be structurally difficult to implement within a VAT framework.

Key Updates That Took Effect in April 2025

ZATCA introduced a series of updates in April 2025 covering application mechanics and exemption categories. These included an expanded definition of taxable transactions to capture borderline cases, an updated electronic procedure for claiming the first-home exemption, and revised penalty schedules. Staying current with these updates is important for anyone entering into real estate transactions - a point our regulatory frameworks advisory monitors continuously for institutional clients.

Which Real Estate Transactions Are Taxable?

Sale, Transfer of Ownership, Gift, and Exchange

All transactions that transfer ownership of real property or a real right over it are subject to the tax: standard sale and purchase agreements, gift deeds transferring ownership without payment, and barter or exchange agreements where the parties swap properties. All of these trigger the tax obligation regardless of whether cash consideration is exchanged.

Long-Term Usufruct Rights Exceeding Fifty Years

The tax does not apply only to full ownership transfers. It extends to long-term usufruct rights exceeding fifty years. This provision targets transactions that transfer effective control and enjoyment of a property for periods that are economically equivalent to ownership transfer, even where formal legal title does not change hands.

Documented and Undocumented Transactions Alike

The tax applies to a transaction regardless of whether it has been formally documented with the relevant authorities. An undocumented transaction does not exempt the parties from the tax obligation. In practice, however, undocumented transactions create additional complications for completing the formal transfer of title, since the property registration process is electronically linked to tax compliance.

What Is the Real Estate Transaction Tax Rate?

The Rate and the Tax Base

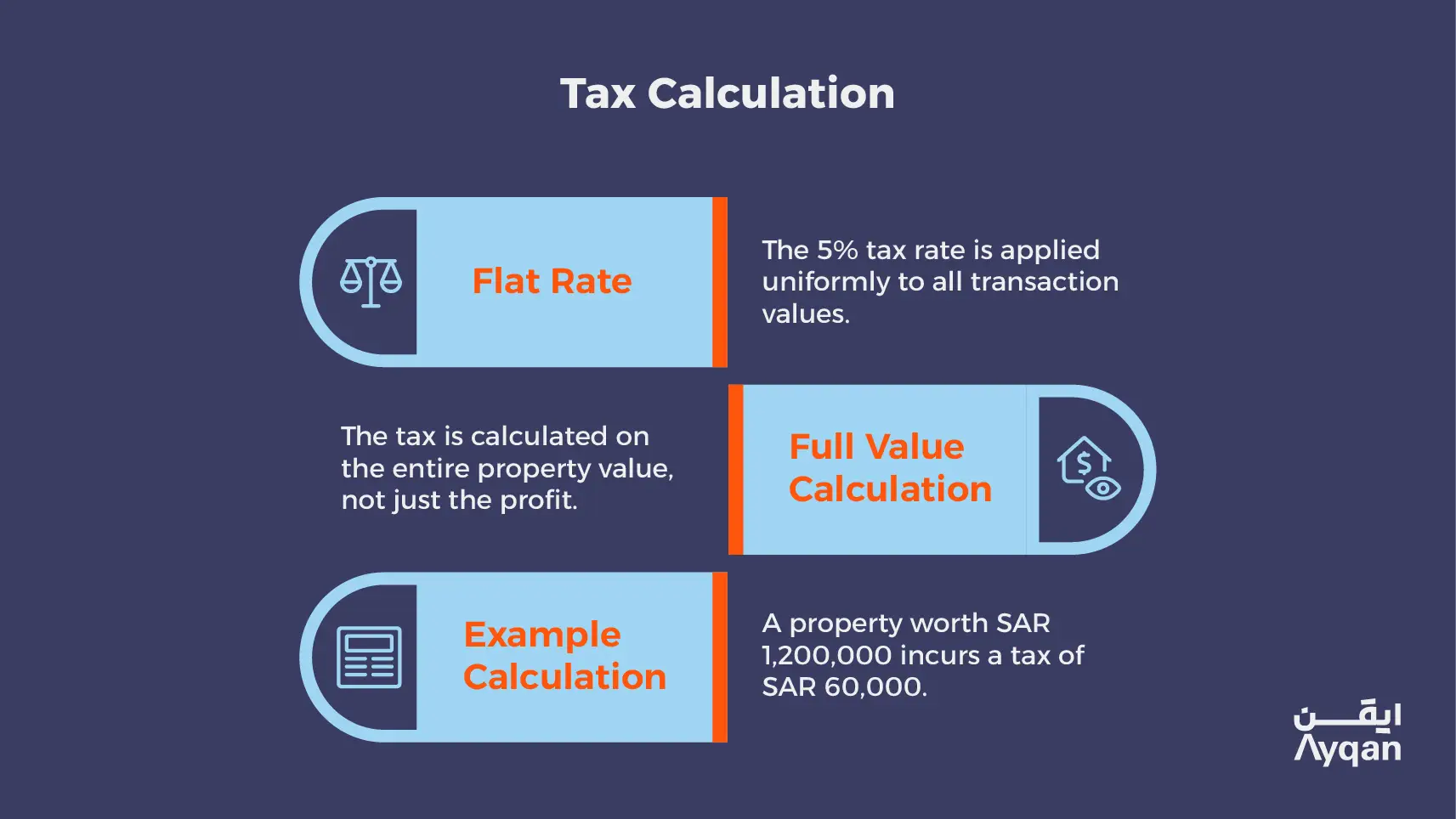

The Real Estate Transaction Tax is calculated at 5% of the full transaction value. In a sale, the tax base is the agreed sale price. Where there is no cash consideration, as in a gift or exchange, the tax base is the market value of the property, determined by ZATCA where the declared value appears understated.

Calculating the Tax on Transactions Above SAR 1 Million

There is no tiered rate or higher bracket for high-value transactions; the 5% rate is flat across all transaction values. On a property worth SAR 1,200,000, the tax is SAR 60,000. One important practical point: the tax is calculated on the full value of the property, not on the profit margin or appreciation from a previous acquisition.

ZATCA's Online Tax Calculator

ZATCA provides an electronic calculator on its official website zatca.gov.sa, where you can enter the transaction value and type and receive an immediate estimate of the tax due. This tool is useful at the negotiation stage of a property deal, allowing both parties to factor the total cost, including tax, into their calculations from the outset.

Who Pays the Real Estate Transaction Tax?

The Seller's Obligation and the Buyer's Exposure

The legal obligation to pay the tax falls on the person transferring the right - the seller, donor, or party disposing of the property. This is the default rule. In practice, however, many sale contracts in the Saudi market contain agreements between the parties to share the tax burden or transfer it to the buyer in exchange for a price adjustment. Such agreements bind the parties as between themselves but do not alter who bears the obligation before ZATCA.

Joint and Several Liability Between the Parties

The Law provides for joint and several liability in certain circumstances: if the seller fails to pay the tax, ZATCA may pursue the buyer, or both parties together. This means a buyer who relies on the seller to handle the payment without verifying it is exposed to collection proceedings. A prudent practice is to verify tax payment or secure it as a condition of completing the transaction - the sort of contractual safeguard our dispute resolution team is regularly asked to enforce after the fact.

The Role of Electronic Registration in Linking Tax Obligations

The electronic registration system ties property transfer to tax compliance automatically. The formal transfer of title and completion of the Ifragha (property clearance) process cannot be finalized through official channels until the transaction has been registered with ZATCA and payment or exemption has been confirmed. This linkage makes tax avoidance technically very difficult.

Exemptions From the Real Estate Transaction Tax

Who Qualifies for an Exemption?

The Law recognizes several categories of exempt transactions: the first home purchased by a Saudi citizen under specified conditions, gifts to relatives up to the third degree, government transactions, certain intra-entity transactions, and specific arrangements under real estate financing structures. Each exemption carries its own conditions and documentation requirements that must be satisfied before the transaction is completed. Our governance & compliance advisory helps institutional buyers document eligibility properly before closing.

The First-Home Exemption: Detailed Conditions

A Saudi citizen is entitled to have the state cover the Real Estate Transaction Tax when purchasing a first residential property, subject to the following conditions: the property must be a ready residential unit (villa, apartment, floor, or duplex), not vacant land and not commercial property; the buyer must not have previously owned a residential property registered in their name; and the buyer must use it as a primary personal residence rather than for rental income.

The state covers the 5% tax on the first SAR 1 million of the property's value, up to a maximum benefit of SAR 50,000. If the property's value exceeds SAR 1 million, the citizen pays the 5% tax only on the amount above that threshold. The exemption certificate (Tahammul Certificate) is issued electronically through the Sakani platform, operated by the Ministry of Municipal, Rural Affairs and Housing in coordination with ZATCA.

Gifts to Relatives Up to the Third Degree

A documented gift of property is exempt from the tax when made between spouses, or to a relative up to the third degree. This covers: first-degree relatives (parents, grandparents and above), second-degree relatives (children, grandchildren and below), and third-degree relatives (siblings, and their children and grandchildren).

The exemption does not apply if the recipient re-transfers the property as a gift within three years to someone who would not have qualified for the exemption had they received it directly from the original donor. Demonstrating the qualifying family relationship requires formally authenticated documentation.

Government Transactions and Compulsory Acquisition

Transactions carried out by government order for public benefit, such as compulsory acquisition for infrastructure projects, are exempt. So are transfers between government entities. This differs from cases where the government sells properties on the open market, which are subject to the general rules.

Intra-Entity Transactions

Certain transactions between entities under common ownership or with a defined corporate relationship may qualify for a reduced tax treatment or exemption under specified conditions. This exception is narrowly defined and requires careful verification with a specialist tax adviser before relying on it.

Financing-Related Exemptions

Finance lease structures (Ijarah Muntahia Bittamleek) executed under real estate finance regulations may benefit from special tax treatment designed to avoid double taxation; the tax is not applied twice - at both the point of contract execution and at the point of final title transfer - in arrangements governed by the Real Estate Finance Law.

How to Register a Transaction and Pay the Tax

Registering Through the ZATCA Platform

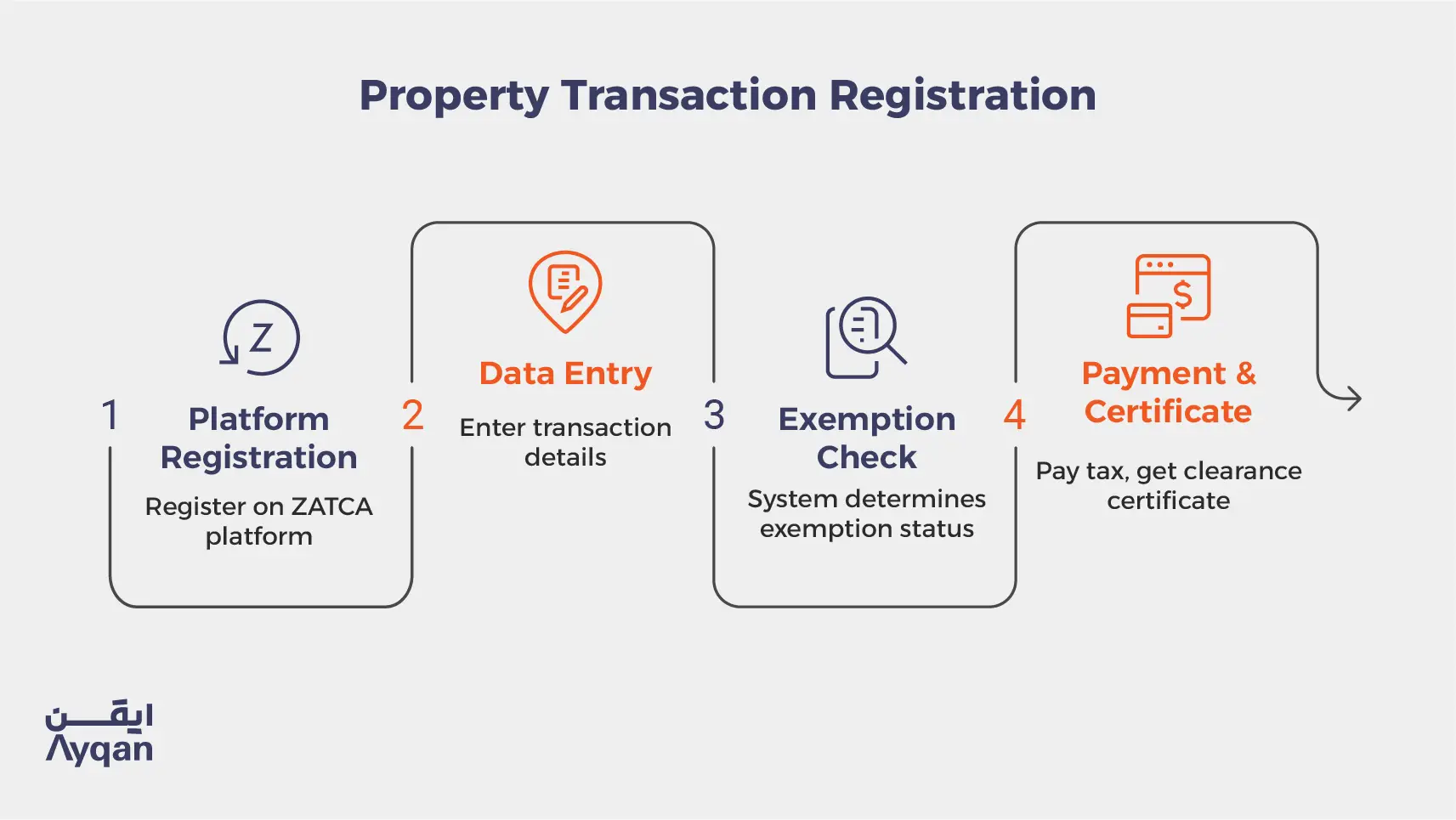

Registration begins on the ZATCA platform at zatca.gov.sa. The applicant enters details of both parties, the property, the transaction value, and the type of transaction. The system then determines whether an exemption applies or whether payment is required. For electronic payment, a clearance certificate is issued that must accompany the transaction documents before formal title transfer.

Obtaining an Exemption Certificate From the Sakani Platform

To claim the first-home exemption, the buyer obtains an exemption certificate from the Sakani platform, operated by the Real Estate Development Fund. The platform automatically verifies eligibility and the satisfaction of the conditions, then issues a digital certificate that is uploaded to the ZATCA registration request.

Accepted Payment Methods

Payment of the tax is made exclusively through ZATCA's approved electronic channels: direct bank transfer or recognized electronic payment gateways. Cash payment is not accepted. This requirement creates a digital record of payment with a precise timestamp that is not subject to subsequent dispute.

Penalties for Non-Compliance

Penalties for Tax Evasion and Late Payment

Tax evasion carries a penalty equal to double the unpaid tax. Late payment after a transaction is completed generates a daily late payment penalty calculated at a specified rate. These penalties can compound significantly if the delay extends over a long period.

ZATCA's Three-Year Retrospective Review Power

ZATCA has the authority to review real estate transactions retrospectively for a period of three years from the date of the transaction. If the review reveals that tax was paid on an understated value, or that an exemption was granted without proper qualification, the Authority may seek the difference plus the applicable penalty. When a review escalates, our dispute resolution and regulatory teams represent clients before the Authority and the tax committees.

Effect of Non-Registration on the Formal Title Transfer

A real estate transaction for which the tax has not been paid and registered with ZATCA cannot complete the formal title transfer process. This means the buyer, despite having paid the purchase price, does not become the legally registered owner until the tax file is resolved. This creates legal uncertainty and risk for both parties.

Should You Get Legal Advice Before Your Property Transaction?

Real estate transactions are among the most financially significant decisions most people make. Verifying the tax position before signing - not after - is essential. Exemption eligibility depends on specific factual conditions that may or may not be satisfied, and complex transactions such as property exchanges and reciprocal gifts require careful analysis to determine the correct tax treatment.

Ayqan provides specialist real estate tax advice and helps you structure transactions to maximize available tax benefits within the legal framework. Book a consultation or contact us through our contact page.

.webp)